Black Sea Presence Looms Larger

A lot of attention has been focused the last few months on actions by the Indian government and how it has disrupted the pulse trade. While that’s certainly the case, other factors that contributed to the Indian government’s decisions seem to have been overlooked. These developments won’t likely disappear either and will remain a large influence in pulse markets.

The main reason behind India’s import tariffs was its large inventories of pulses that weighed on domestic prices and raise the ire of farmers there. Larger domestic production was one reason behind these heavy inventories but a sharp rise in imports was the main source of supplies.

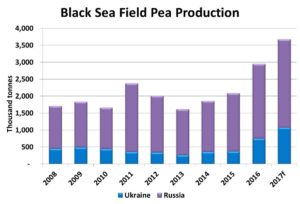

The oversupply of pulses actually began with the large 2016 crops that were grown in many countries, including Canada, the US and Australia. But in 2017, all three of these exporters reduced production either through fewer acres or lower yields. Not everyone was reducing production however. In the Black Sea region, pulse production continued to ramp up even further in 2017. For Russia and Ukraine combined, pea production was up 41% in 2016 and another 24% in 2017.

And it’s not just peas; farmers in these countries are looking for opportunities to diversify, just like in Canada. Production of chickpeas and lentils has also expanded rapidly, helped by the high price environment of the previous two years. In addition to Russia and Ukraine, Kazakhstan has been increasing pulse production. For example, one report indicated Kazakh lentil area has jumped from 17,000 acres in 2014 to over 800,000 acres in 2017.

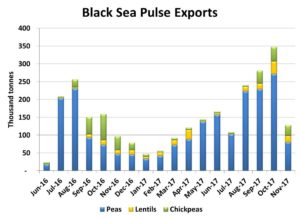

Because the pulse harvest in parts of the Black Sea region typically starts a few weeks earlier than western Canada, these countries were able to get a head start on shipping to India. While not all of the pulses were headed to India, large volumes were able to move prior to the Indian import tariff on peas in November. And their entry into that market was a big (but not the only) reason why India decided to restrict imports.

While seeded area of pulses in the region will likely decline in 2018 due to lower prices, these countries won’t disappear from the picture either. Competition has also been increasing from countries in the Baltic region and eastern Europe and that’s a new market reality. But all is not lost; there are things that Canada can do to remain competitive.

A focus on quality is more important than ever. Currently, Canadian pulses hold a premium over Black Sea product due to consistency and quality. To maintain that lead, the Canadian production and handling system needs to adapt around meeting customer needs. In addition, developing new markets and strengthening relationships with existing customers remains critical. Varietal and agronomic research is also needed to continue providing Canadian farmers with a competitive advantage.

Development of a domestic pulse processing industry is probably the best way to diversify markets and reduce risk. This would also mean less of Canadian pulse crops need to compete head-to-head in export markets. Canada’s canola crushing industry is the best example of this type of strategy, where nearly half of Canada’s canola is now crushed domestically. Because of increased export competition, it’s worth pursuing a similar direction for pulses.

Pulse Market Insight provides market commentary from Chuck Penner of LeftField Commodity Research to help with pulse marketing decisions.