Opportunity and Risk in Pulse Markets

Uncertainty is certain in crop markets. The unpredictability starts with the weather, but there are many other sources of uncertainty. Some developments can result in positive opportunities for markets while others add to the downside risk for prices. It’s just as important to be aware of the potential risks as the more promising possibilities.

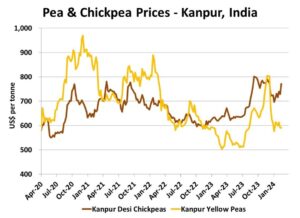

In late 2023, the yellow pea market got a boost from the news that India was suspending its import tariffs on yellow peas for the first time in years. The only problem is the deadline of March 31, which limits the movement of peas to a couple of months and is now winding down. The main uncertainty (and opportunity) for the yellow pea market is whether the Indian government will decide to extend this deadline past March 31.

There are a few reasons why the zero-tariff deadline could be kept in place beyond March 31. A general election in India is scheduled for Apr-May and food inflation is a large issue for consumers. The Indian government has extended zero import tariffs for other pulses, which suggests a real concern about boosting pulse supplies and keeping food prices under control. In recent weeks, prices of desi chickpeas (which yellow peas replace) in India have started turning higher again. Fewer acres of desi chickpeas have been planted in India, raising concerns about a smaller harvest in 2024.

These various factors are raising the odds that the zero import tariffs could be extended but that’s still far from certain. Indian farmers are staging demonstrations with higher prices a key demand, and it’s not clear how the government will respond with trade policy. If the zero tariffs are extended, it would be positive for yellow pea prices, both for the rest of 2023/24 and into 2024/25.

There are also some immediate opportunities in green pea and green lentil markets with record prices in 2023/24, although those are only available for those farmers still holding onto old-crop supplies. New-crop bids are also exceptionally strong, which offer opportunities to lock in solid profits on the 2024 crop.

The positive situation for green peas and green lentils also presents some risks. The strong prices will very likely encourage more acreage of these crops in Canada. Farmers in places like the US and Kazakhstan are also seeing the same price signals and will likely boost their plantings. More production increases the risk of lower prices, especially since demand for green peas and green lentils tends to be fairly stable.

The red lentil market seems to be facing more risk than opportunity, particularly the risk of weaker Indian demand. Earlier this year, India was Canada’s main destination for red lentil exports, but those volumes dropped sharply in December. And that situation could continue.

Indian farmers have planted record acreage of red lentils and growing conditions have been decent. With the rabi harvest about to start, there is potential for a record lentil crop which could cause prices to fall and imports to drop. With more competition from Australia and poor demand from other importers, a drop in Indian buying would not be helpful for Canadian red lentil prices. That’s especially the case since exports to other countries have lagged this year.

As always, the weather is the biggest influence on pulse markets and can easily override any of these opportunities or risks. The dry conditions in western Canada are a critical concern and are likely the largest risk of all.

Pulse Market Insight provides market commentary from Chuck Penner of LeftField Commodity Research to help with pulse marketing decisions.