First StatsCan Crop Estimates for 2025

This week, StatsCan issued its first yield and production estimates for 2025 crops. These numbers are based on computer models using satellite vegetation images which, in our view, have been getting better at estimating yields. That said, these first estimates were based on the situation at the end of July; weather and crop conditions have changed considerably since then, some worse but mostly better.

As combines got rolling this fall, one common theme we’ve been hearing from many parts of the prairies has been that yields are coming in better than expected. Rainfall was variable across the prairies but in all regions, 2025 was a much milder summer than the last 3-4 years when extended periods of extreme heat reduced yields. If these early positive results continue through the rest of harvest, we wouldn’t be surprised if these initial StatsCan numbers are the low-water mark for the season.

For peas, StatsCan reported a yield of 36.6 bu/acre, up from 34.8 bu/acre last year and about three bushels better than the 5-year average. This higher yield, along with a 9% increase in seeded area would result in a 2025 Canadian pea crop of 3.41 mln tonnes, 400,000 tonnes (14%) larger than last year and the biggest crop since 2022/23. Back in June, StatsCan’s acreage estimates showed yellow pea area expanded the least, with larger gains for green and especially “other” peas, which includes maples.

In a normal year, this size of production increase could be absorbed by the market without too much difficulty, but 2025/26 isn’t normal for peas. Import tariffs by China, Canada’s largest customer, will restrict export potential and it will be difficult to find a home for that lost tonnage in other countries. Ultimately, 2025/26 ending stocks could end up at historically high levels.

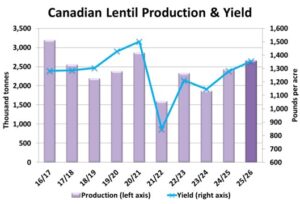

StatsCan reported positive yields for lentils in 2025. Its estimate of 1,355 pounds (22.6 bushels) per acre was the highest since 2020/21 and, based on early harvest results, could still be too low. The improved yield, along with a 4% increase in seeded area, would mean a lentil crop of 2.66 mln tonnes, 225,000 tonnes (9%) larger than last year. And with a larger old-crop carryover, 2025/26 supplies could be in record territory. Keep in mind that back in June, StatsCan reported large increases in green lentil acreage while seeded area of reds actually declined. This suggests a sizable shift in Canadian lentil supplies toward greens while red lentils don’t appear as burdensome.

The lentil export market isn’t facing hurdles as serious as those for peas, but there are issues. Back in March, India imposed 10% tariffs on lentil imports which hasn’t stopped trade but does require discounted prices. Even so, Canadian red lentil exports could expand in 2025/26. The greater concern could be dealing with the large supplies of green lentils, with global trade tending to be more-or-less static.

StatsCan was more cautious with its estimate of chickpea yields, reporting output at 1,289 pounds (21.5 bushels) per acre, the lowest yield since 2021/22. Even with a lower yield, the 13% increase in seeded area would mean a 2025 chickpea crop of 309,000 tonnes, 8% more than last year. If yields end up close to this initial StatsCan estimate, 2025/26 supplies won’t be huge but still quite comfortable. Canadian chickpea exports have been strong for the last year and performance could be strong again in 2025/26, keeping stocks from feeling too heavy.

The StatsCan production estimate for dry beans show 2025 production at 353,000 tonnes, down 16% from last year. This is mainly due to a yield of 2,160 lb/acre, the lowest since 2021/22. That said, there are sizable questions not only about its bean yield but also StatsCan’s seeded area estimate, which could be understated by nearly 50,000 acres.

As always, these estimates are subject to debate. The next StatsCan model-based estimates will be released in only a few weeks, based on August conditions. Yields and production numbers will see changes, quite likely higher. The “final” crop estimate will be released in early December based on a farmer survey, but even that is prone to questions and debate.

Pulse Market Insight provides market commentary from Chuck Penner of LeftField Commodity Research to help with pulse marketing decisions.