US Acreage Implications

While we wait for the StatsCan Seeding Intentions report later this month, we can get a sneak peek at what farmers are thinking, at least in the south of the border. The USDA recently released its Prospective Plantings report with 2018 acreage forecasts for pulses. There are certainly some parallels between pulse crops on both sides of the border, but there are also differences in the two situations.

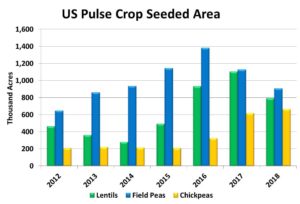

Farmers in the US told the USDA they would be cutting pea acreage to 908,000 acres, down 20% from last year. But just because plantings are down 220,000 acres, there won’t be a corresponding drop in production. Last year’s drought cut US pea yields to 22.5 bu/acre and a recovery back to average yields would more than offset the reduced acreage. Normal yields would mean a 2018 crop of 700,000 tonnes compared to 640,000 last year.

Bids in the US for yellow and green peas are only a few cents apart, in contrast to Canada where average green pea bids are holding a $1.50 (or more) per bushel premium over yellows. This means that in the US, there won’t likely be a shift out of yellow peas and into greens like we’re expecting in western Canada. That said, green peas in the US already make up roughly 40-45% of total acreage. This means the US will continue to be a competitor in both the green and yellow pea markets.

Lentil acreage in the US is expected to drop even harder than peas. The USDA is projecting a 28% decline in lentil acreage, dropping to 790,000 acres from last year’s record. But just like peas, that drop in acres won’t turn into a much smaller crop. If US lentil yields recover from last year’s dismal performance and get back to average, the 2018 crop would actually be 410,000 tonnes, 21% better than last year and the second highest on record.

US lentils are mainly green types, particularly medium greens. The drop in acreage is helpful but if the crop size actually increases in 2018, it will mean heavier competition in green lentil export markets, as there’s often some substitution between the various sizes. In western Canada, we’re hearing that 2018 green lentil acres will actually be higher than a year ago and that raises the potential for a much larger North American supplies and won’t be friendly for prices. Red lentil markets will be almost completely unaffected by the situation in the US.

The one pulse in the US that is expected to see increased seeded area is chickpeas, with 7% more acres than last year. This seems like a relatively small increase but when that’s combined with a rebound to average yields, the 2018 crop could be as much as one-third larger than last year.

Because the US is Canada’s largest customer for chickpeas, a larger domestic crop there would limit demand for Canadian chickpeas. Seeded area of chickpeas is also expected to be up in western Canada, which could turn into very heavy North American supplies. The one caution on both sides of the border is the late spring which, because of the long growing season, could affect chickpeas more than other crops.

The USDA also issued an estimate for dry bean acreage at 2.03 mln acres. That’s down 3% from last year, but chickpeas (garbanzos beans) are included in that total. If we strip chickpeas out of that total, US dry bean seeded area would end up at 1.37 mln acres, down 7% from last year. That has the potential to provide a little upside potential for dry bean prices in 2018/19.

Pulse Market Insight provides market commentary from Chuck Penner of LeftField Commodity Research to help with pulse marketing decisions.