What’s Waking up the Pea Market?

Most pulse markets have been pretty sleepy through the winter, caused by the slowdown in Indian demand and large global supplies. A few, such as lentils, have been worse than sleepy, seemingly slipping into a coma. Pea markets have also been a little drowsy earlier this year but are now showing some signs of life.

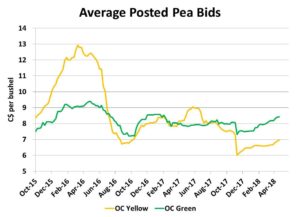

Prices for both yellow and green peas have been moving higher in the last few weeks, with greens holding onto a sizable premium. The average bids shown in the chart don’t fully reflect the strength in the market. For example, the top end of the range for green peas is around $9.00 per bushel and $7.25 is available for yellows in some locations. New-crop bids are solid as well.

There are a few factors that have helped peas shrug off the weakness in other pulse markets. For green peas, supplies were already on the low side at the beginning of 2017/18. Last year’s seeded area in western Canada had shifted more toward yellows and a couple of years of low green pea production finally caught up to the market. It also helped that other countries which had scaled up production mostly did it with yellow peas, leaving less competition in the green pea market.

More importantly, the import tariffs imposed by India had very little impact on the flow of green peas. Even though the tariffs were applied against all types of peas, prices for green peas within India rose so sharply when the tariff was announced that there was no real slowdown in Indian imports. In addition, Canadian green pea exports aren’t quite as dependent on the Indian market and other countries have continued to buy at a steady pace. At the time of writing, it’s still not clear whether India’s latest three-month import ban on peas applies to green peas but even so, it won’t have a long-term effect.

The bottom line for green peas is that global supplies for 2017/18 are actually fairly tight and are getting tighter as the year moves into its late stages. And export demand also hasn’t slowed down to any degree, allowing prices to move higher.

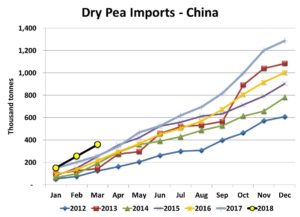

Yellow peas were affected more by Indian tariffs but even before that, global supplies were already heavy. With large inventories of yellow peas, the only real price support comes from increased demand. With India largely out of the picture, the dominant buyer has been China. Chinese imports late in 2017 were very strong, taking annual volumes to a record of 1.29 million tonnes. The first quarter of 2018 has also been running at a record pace which has helped relieve the burdensome supply situation.

More recently, reports have circulated that China’s threat to impose a tariff on US soybeans has triggered Chinese purchases of other feed protein sources, including peas. This would be additional demand beyond the peas used for fractionation. This development hasn’t shown up in the trade data yet but would help push demand to even higher. Add to that some market rumours that Indian buyers are still asking about Canadian yellow peas in early fall is helping add some price support.

These are positive developments for the pea market which has faced a lot of negative publicity over the past few months. It also creates a brighter picture for the 2018/19 pea market. The only danger is getting too excited about prospects, especially for greens, and oversupplying the market again.

Pulse Market Insight provides market commentary from Chuck Penner of LeftField Commodity Research to help with pulse marketing decisions.