How Big Are the Pulse Stockpiles?

Based on some of the amped up talk about Indian pulse tariffs and how they’re restricting Canadian exports, you’d think there’s no end to the big supplies of pulses on Canadian farms. That’s not to say there hasn’t been a serious impact on Canadian exports, but the supply situations are quite mixed for the different types of pulses.

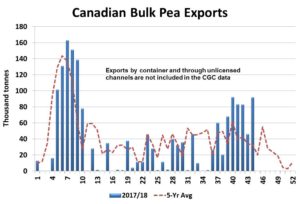

This week, StatsCan released its export data for April and pea exports were shown to have jumped to 346,000 tonnes after a string of mediocre months. And the weekly data from the CGC shows an unusual flurry of export activity in May, extending the April streak. It’s true that pea exports are still well behind last year’s record pace but thanks to Chinese buyers, the outlook for peas is looking a little brighter.

Overall, this late-season improvement in pea exports is helping trim estimates for 2017/18 ending stocks. Earlier in the year, there were some suggestions there would be over a million tonnes of peas left at the end of 2017/18. Now, it’s looking more like pea ending stocks will be around 600,000 tonnes. That’s still large, but lower than a few other years when stocks were much more burdensome.

When we look at export performance of green peas specifically, we see there’s been no drop-off at all this year. That includes India, which has continued to buy green peas. In fact, Canadian green pea exports for Aug-Apr are 220,000 tonnes, ahead of last year at 205,000 tonnes. The result is that green pea ending stocks are becoming quite tight, as evidenced by some $9.00 per bushel bids.

This improved stocks situation is also positive for the 2018/19 outlook. Because fewer old-crop peas will be carried forward into the next marketing year, those supplies won’t be as heavy either. Of course, a lot depends on this year’s yield outcomes which are still far from clear. The acreage split between yellows and greens is also an important factor. Even so, it’s possible Canadian pea supplies could actually start to look tightish in 2018/19, which would be a fairly quick turnaround from this year’s doom and gloom.

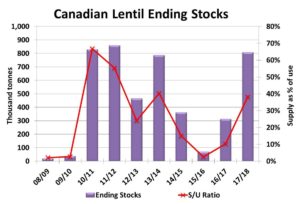

Unfortunately, the same cautiously optimistic outlook doesn’t apply to lentils. While there’s been some improvement in Canadian exports the last couple of months, it’s still not enough to make a significant dent in Canadian lentil supplies. That said, I’m not quite as pessimistic as some reports that suggest 2017/18 lentil ending stocks could be around a million tonnes. Still, our current ending stocks estimate of 750-800,000 tonnes is back up to the levels seen a number of years ago, when lentil bids were even a bit lower than they are now.

One of the differences for lentils (compared to peas) is that there isn’t a “China” waiting in the wings to scoop up large supplies. Canada is still heavily dependent on India, especially for red lentils. That means it would likely take a crop failure there to turn the market higher and, at the earliest, that wouldn’t be evident until early 2019, if at all.

Of course, a problem with the Canadian lentil crop would also “help” the supply situation, but that’s not something we’re counting on either. Even if that happened, carrying over 800,000 tonnes of old-crop lentils would soften the impact of a smaller 2018 Canadian crop. This means that unless there’s a serious crop production problem somewhere, the lentil market will remain under pressure for longer than peas.

Chickpeas and dry beans aren’t facing the same type of large ending stocks, due to strong export programs. In fact, the 2017/18 marketing year will end up with very few chickpeas or beans left in farmers’ bins or traders’ inventories. Chickpea production is expected to rebound significantly, replenishing supplies, but dry bean supplies could get even tighter in 2018/19.

Pulse Market Insight provides market commentary from Chuck Penner of LeftField Commodity Research to help with pulse marketing decisions.