What Do the StatsCan Survey Results Mean?

On August 31, StatsCan released its first yield and production report, based on a survey of roughly 13,000 farmers. That’s a large enough survey sample to give fairly reliable results, but there’s always some question about the numbers.

Keep in mind, the phone survey in occurred from July 6 to August 1, so the answers farmers gave reflected their views before they actually got into the field. And prior experience tells us that even experienced farmers can be surprised (both higher or lower) with how crops end up yielding. With that disclaimer, we’ll be dissecting the implications of the yield estimates as they were reported.

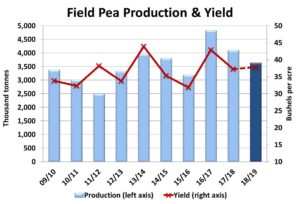

For peas, StatsCan reported a crop of 3.635 million tonnes, 12% smaller than last year. The yield was pegged at 37.8 bu/acre, slightly above last year’s 37.2 bushels, but a bit lower than the 5-year average yield of 38.2 bu/acre. This production total wasn’t really a surprise, as the average trade guesstimate was 3.5 mln tonnes.

In the next few days, StatsCan will also be releasing its estimates of July 31 stocks. The combination of those old-crop inventories and this 2018 production estimate will set the stage for 2018/19 supplies. For the most part though, we’re expecting 2018/19 to be fairly well-balanced for peas, in spite of the dim outlook for exports to India. As a result, we don’t look at this 3.6 million tonne crop as making the outlook heavy or adding any (more) pressure to prices.

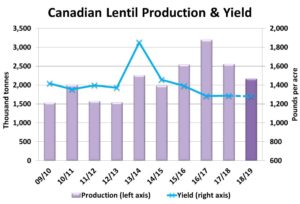

The lentil production estimate from StatsCan came in at 2.17 million tonnes, 15% smaller than last year. The yield was estimated at 1,280 pounds (21.4 bushels) per acre, almost identical to the past two years but lower than the 5-year average of 1,450 pounds per acre. This total is slightly lower than the average trade guess of 2.3 million tonnes and would be the smallest crop since 2014/15.

The problem for lentils is that the old-crop carryover from 2017/18 will likely be quite high. Even with this drop in production, 2018/19 supplies could actually end up larger than last year. And with clouds still hanging over the export outlook, supplies will feel heavy again. This production estimate certainly doesn’t hurt the market tone, but the crop total wasn’t small enough to really provide much optimism either.

The 2018 chickpea crop was estimated at 264,000 tonnes. StatsCan trimmed some acreage but also reported a yield of 1,333 pounds per acre. According to StatsCan, that yield is slightly higher than last year, but we know the 2017 crop had been seriously underreported. Even with these lower than expected results, the crop is still 176% larger than StatsCan’s estimate for last year (which was far smaller than reality). Regardless of the exact increase, the Canadian crop is much larger than last year at the same time as supplies in other countries are feeling burdensome. Recent bids already reflect this pessimistic outlook.

StatsCan’s estimates for dry beans are always a little tricky as the acreage totals are often different than what the provincial crop insurance data tells us. In any case, StatsCan reported a 308,000 tonne dry bean crop for 2018, 4.5% smaller than last year. For dry beans, this would be fairly supportive, especially in light of reduced dry bean acres in the US, the dominant influence on Canada’s market.

Pulse Market Insight provides market commentary from Chuck Penner of LeftField Commodity Research to help with pulse marketing decisions.