How are Lentil Supplies Looking?

In the last Pulse Market Insight, we looked at pea supplies in 2019/20 with a bit of concern. The lentil situation is similar. Just like peas, we were surprised this spring to see that low lentil prices hadn’t done anything to discourage acres, with seeded area unchanged from 2018. That seems to suggest pulses are quite fixed in farmers’ crop rotations and it will take more than low prices to cause acres to drop.

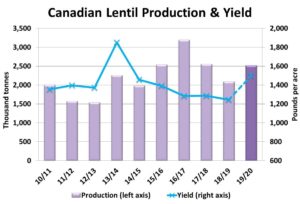

Besides the acreage number, the latest StatsCan production estimate is showing the 2019 lentil yield at just under 1,500 pounds (25 bushels) per acre, the highest yield since the bumper crop of 2013. The result is a 2019 lentil crop of 2.5 mln tonnes, 20% more than last year.

It’s important to break that number down a little more though to understand the implications. After all, there are a number of distinct submarkets for lentils. According to StatsCan’s acreage numbers, green lentil production would only be up 2% from last year while the red lentil crop would be 34% larger than last year. On the surface, that looks a lot heavier for reds than greens but the old-crop carryover (from 2018/19) for reds was down considerably more, which offsets most of the production increase. In total, 2019/20 supplies are forecast at 3.2 mln tonnes, 7% more than last year and the second-highest on record.

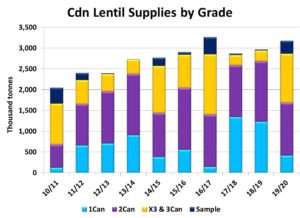

There’s also the quality angle to consider. The serious delays in the 2019 harvest have downgraded the lentil crop significantly. If we look at the earlier years (2010, 2014 and 2016) when harvest was also very slow and pencil in those years’ grades, only 40-45% would end up in the top two grades compared to the long-term average of 70-75%. Even when we add in the better quality carryover from the past couple of years, it’s clear supplies of 1Can and 2Can lentils will be significantly lower than most years.

On the surface, the lower 2019 grades appear negative (specifically for farmers who got the lower grades), but they just might help with total lentil consumption. For one thing, a number of overseas buyers are price-sensitive and could take more lentils if the quality and price fit the bill. The domestic feed market may also chew through more sample grade lentils and reduce the stockpiles.

So far, our projections are calling for roughly steady lentil exports until we see more evidence of stronger demand. We have raised our estimate of domestic feed use though. The bottom line result is a 2019/20 ending stocks forecast of just over 600,000 tonnes, down slightly from last year but essentially a similar outlook.

Pulse Market Insight provides market commentary from Chuck Penner of LeftField Commodity Research to help with pulse marketing decisions.