Prices Decline to Find More Demand

In the last Pulse Market Insight, we talked about how high prices restrict demand to only those customers willing to pay more. As prices rise, they weed out the more price sensitive buyers until only a few remain at the top of the market. This has been happening for most pulse crops in 2021/22, with prices climbing to multiyear highs for some and record levels for others.

That’s the good news behind this behaviour of “demand rationing”, as stronger buyers push the market higher. We’ve seen this happening in the first few months of 2021/22, especially from the US, where users of peas and chickpeas aggressively bid the market higher. The downside occurs once that high-priced demand has bought enough to cover its needs. Then only the more price-sensitive buyers are left.

One way to picture this type of market environment is to think about a pyramid. High prices are the peak of the pyramid, but that’s also where the volumes sold are the smallest. To encourage more demand, prices need to drop down into the next tier, which seems to be happening now with pulse prices. Of course, the market is more complex than simply three levels shown in the diagram; the reality is that it’s more of a sliding scale.

The tricky part is figuring out just where the various price levels are that trigger more buying and how much new demand shows up at various prices. This “price discovery” process is happening now in peas, lentils and chickpeas. As prices decline, it becomes more difficult (but not impossible) for prices to rebound back up to the old highs, unless the high-priced demand returns with fresh purchases or the mid-level buyers change their mind about how much they’re willing to pay.

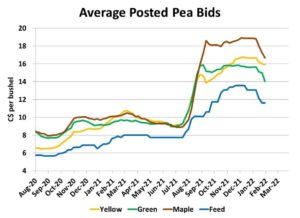

For peas, the US demand at the top of the pyramid now seems to have been filled. Even though Canadian pea supplies in 2021/22 are the lowest in years, there are still some other peas left to sell. Prices are now moving lower to find that next tier, likely from China or to a lesser extent Cuba. That has allowed bids in western Canada to slide, with more motivated farmer selling adding to the declines. This tier of demand is likely large enough to use up the rest of Canadian pea supplies. At the low end of the pyramid are the most price-sensitive buyers, largely from South Asia, but supplies aren’t big enough that prices will need to fall that far in 2021/22.

It’s a similar picture for lentils, with bids in western Canada declining to try to uncover more demand. Buyers are still out there but they’re not as concerned about locking in supplies. That’s especially the case for red lentils with Australian supplies already available and the Indian harvest coming in a few weeks.

For chickpeas, the situation is almost the same as yellow peas. The high prices paid earlier came from US demand but now that these buyers have enough coverage, bids are sliding to trigger purchases from more price-sensitive countries in Asia and the Middle East.

The pyramid example also applies to new-crop markets. If there’s improved moisture in 2022 and supplies expand, trades will shift down to the middle and lower price tiers, depending just how large the 2022 crop is. On the other hand, if crop conditions don’t recover and volumes are small, we’ll once again be operating in the higher end of the pyramid.

Pulse Market Insight provides market commentary from Chuck Penner of LeftField Commodity Research to help with pulse marketing decisions.