Added Uncertainty in Pea Markets

At this time of year, farmers are nailing down the last few decisions about their cropping mix. In the past few months, pulse markets have experienced some serious volatility, starting with last summer’s drought cutting back yields in a big way. Beyond that, severe difficulties with shipping and economic turmoil in several key destinations have made 2021/22 a year like no other.

Now, we’re trying to provide some reconnaissance and see how things could unfold in the coming months and into 2022/23. Although certain factors, most notably the weather, are difficult to predict, we also look to other parts of the world for events that will influence pulse markets.

This year, besides the usual unknowns about weather, there’s the additional turmoil occurring in the Black Sea. For the pea market (and others), there are two questions raised by Russia’s invasion of Ukraine, one short-term and one longer-term. Just to be clear, we hardly need to state that the issues for Canadian pulse growers are far less dire than those facing farmers in Ukraine.

In the short-term, vessel movement out of Black Sea ports has been disrupted and has forced shipping to be cancelled or (where possible) rerouted. This halt in sea shipping, along with shutdowns in financial systems have added large risks and made traders hesitant to make deals.

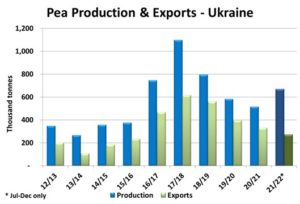

These short-term disruptions have caused large price volatility for certain crops but have less impact on pea markets. The main reason is that most peas, the main pulse exported by Ukraine and Russia, have already moved out of the region. Three quarters of the Ukrainian export program was already complete by the end of December and even more would have been shipped by the end of February, leaving relatively few unshipped peas.

There are still more Russian peas left to export but getting them to customers may prove difficult. So far in 2021/22, Russian pea exports are running at a record pace of 934,000 tonnes, with another 500,000 tonnes possible in the final five months of the marketing year. Generally, customers buying Russian peas are fairly price-sensitive. Because of this, we don’t expect to see them switch to Canadian peas and trigger a noticeable surge in demand.

The ability of Ukrainian farmers to get the 2022 pea crop planted is the longer-term and larger potential impact of the Black Sea turmoil. Planting of the pea crop would normally be underway already, but farmers in Ukraine are facing serious obstacles. The heaviest concentration of pea acres is in the south and southeast of the country, where fighting is intense.

One estimate from a Ukrainian analyst suggested nearly 40% of spring-seeded crops would not get planted. Because of when and where they’re planted in Ukraine, that percentage for peas would likely be even higher. If that’s the case, production in 2022/23 could easily be cut by more than half and would reduce export availability.

In a more normal year when global inventories are comfortable, the loss of a few hundred thousand tonnes of peas wouldn’t have a large impact. But because supplies look like they’ll be tight again in 2022/23, the market will notice their absence. The largest impact will be in the European market, the largest destination for Ukrainian peas, but the ripple effects will tend to support prices elsewhere. Sadly, this is another case of the unfortunate truth that one set of farmers benefit from the misery of others.

Pulse Market Insight provides market commentary from Chuck Penner of LeftField Commodity Research to help with pulse marketing decisions.