Indian Crop Estimates and Price Signals

A few weeks ago, the Indian Ag Ministry released its latest 2022/23 crop estimates, including its first look at production during the rabi (winter) season. The Indian rabi crop includes the main pulses of interest for Canadian farmers, chickpeas, peas and lentils. At this time of year, the rabi harvest is in its early stages and final estimates will change once those results are known. For now, these should be viewed as just early ideas.

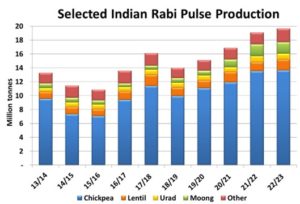

Total rabi pulse production is estimated at 19.65 mln tonnes, up 3% from last year and another record. In general, this isn’t a complete shock. Total pulse seeded area has been reported as a bit above average and growing conditions have generally been favourable for most (but not all) of the growing season across the country.

Looking separately at the more relevant pulses, production of chickpeas (mainly desi but also kabuli), production is estimated to be up less than 1% at 13.6 mln tonnes. The lentil crop is reported at a near record of 1.6 mln tonnes, 26% more than last year. That’s based on a 5% increase in seeded area and a recovery in yields. The Indian pea crop isn’t reported separately but fits in the “other” category of rabi pulses which is up 18% from last year.

As with government crop estimates in every country, there’s plenty of skepticism and second-guessing. In India, there’s frequent criticism that the numbers are too optimistic to paint a rosy picture of supplies for the general public and hopefully keep a lid on prices. That may or may not be true but, even before this government report, prices were already responding to signals from within India. And of course, external events have also contributed to price direction.

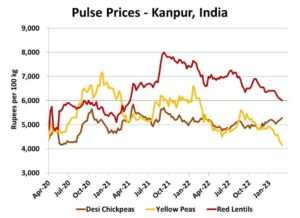

In the case of red lentils, Indian prices have been sliding for several months and are now at the lowest level since March 2021, prior to the Canadian drought. The latest declines can be attributed to a combination of ideas about India’s larger rabi crop and an increase in Australian production.

There hasn’t been the same type of pressure on desi chickpea prices, largely because the Indian crop isn’t expected to expand much and old-crop supplies are reported to be on the snug side. While not shown on the chart, kabuli chickpea prices have dropped sharply in the last week or two as there are ideas that this part of the Indian chickpea crop expanded this year.

Yellow peas are the weakest part of this price chart, already under pressure but dropping sharply since mid-January. Even though we don’t have an official estimate of the upcoming pea crop, it’s clear the Indian market isn’t concerned about supplies.

Even though there may be questions about the reliability of the crop estimates, the price signals seem to confirm the general direction of pulse production. If the combination of Indian desi chickpea and pea crops is larger, it suggests the odds are very low the Indian government will lower its restrictions on pea imports anytime soon. That said, this isn’t really “news” and doesn’t change the outlook for Canada’s pea market. For lentils, the crop estimate and price behaviour suggest India won’t be a driver of stronger markets over the next several months.

Pulse Market Insight provides market commentary from Chuck Penner of LeftField Commodity Research to help with pulse marketing decisions.