Risks Ahead for Yellow Peas

Canadian agriculture is heavily dependent on exports; that’s inescapable. This country has abundant resources relative to its population and that’s especially the case for agriculture. For pulse crops like peas and lentils, Canada frequently exports 90% of its annual production, so what goes on outside its borders is critical to success.

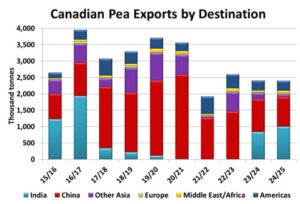

Lately, there’s been a lot of talk about possible trade glitches with some of Canada’s key trading partners. Looking at peas, the chart shows Canadian exports over the last 10 years and clearly reveals how much is riding on just two countries, India and China.

The largest question mark for peas is the situation in India. The chart reveals how Indian tariffs and quantitative restrictions on pea imports, which were imposed late in 2017 and only rolled back in December 2023, affected Canadian trade. While those tariffs were in place, Canada relied even more heavily on China as a destination. Once those tariffs were rolled back, Canadian exports remained dominated by only two countries.

The cloud hanging over the pea market now is that India’s zero tariffs on yellow peas have a deadline of December 31, at which time India could reimpose tariffs. That deadline has already been extended twice, and there is a chance this could happen again. If so, it would mean Canadian yellow peas will continue to have solid movement through the rest of 2024/25 and the market would remain supported.

But if India decides to put tariffs back on imports, Canadian yellow peas will have a harder time finding a home in the second half of 2024/25. When India imposed tariffs back in 2017, there wasn’t much competition in the Chinese market and Canadian peas were imported for both food/fractionation usage and feed consumption. In the last two years though, Russia has become a strong competitor in China, and Canada are no longer “owns” that market, making it more difficult to increase exports there.

India’s decision about tariffs on yellow peas will largely hinge on the situation with its rabi crops, which are now being planted. Moisture has been plentiful across much of the country, which should mean good conditions for establishing crops. In some areas, excess moisture has caused some planting delays but that’s not a large concern yet. In addition, the Indian government has raised Minimum Support Prices (MSP) for chickpeas and lentils, which could encourage pulse plantings.

On the other hand, there have been reports that Indian farmers could switch some rabi pulse acreage to wheat. The MSP for wheat was also raised and market prices are at record highs, which could make wheat a more attractive option, especially since wheat is grown in some of the same areas as chickpeas, peas and lentils. If the competition for acres swings toward wheat, the prospect of smaller pulse crops could encourage the Indian government to keep allowing imports.

Prices are the other factor that will influence the government’s decision. Currently, Indian prices for both yellow peas and desi chickpeas have been very weak. If the government decides it wants to use import restrictions to support farmers’ incomes, it could reimpose tariffs to try to boost domestic prices.

While the situation for yellow peas is still somewhat uncertain, there is considerable risk if India shut its borders. And the window of opportunity may be closing. The good news is that Canadian pea exports have been exceptionally strong so far in 2024/25, with good opportunities for farmers to move their peas. And for green peas, Canadian exports don’t depend on India as a buyer. Global demand for green peas has been very strong and will continue to be solid throughout 2024/25.

Pulse Market Insight provides market commentary from Chuck Penner of LeftField Commodity Research to help with pulse marketing decisions.