StatsCan Pulse Acreage Numbers (Mostly) Not Surprising

The first official forecasts of 2026 seeded area were recently issued by StatsCan, with some “interesting” estimates for a few crops. For pulse crops though, most of the acreage numbers weren’t really out of line with expectations.

It’s important to note that even though StatsCan’s estimates were issued in early March, they were based on a farmer survey that occurred between mid-December and mid-January. Since that survey, there have been sizable market developments that could influence acreage decisions. That said, crop rotations are largely fixed and a portion of the acreage was already decided back in December. But there is still room for some late tweaking around the margins.

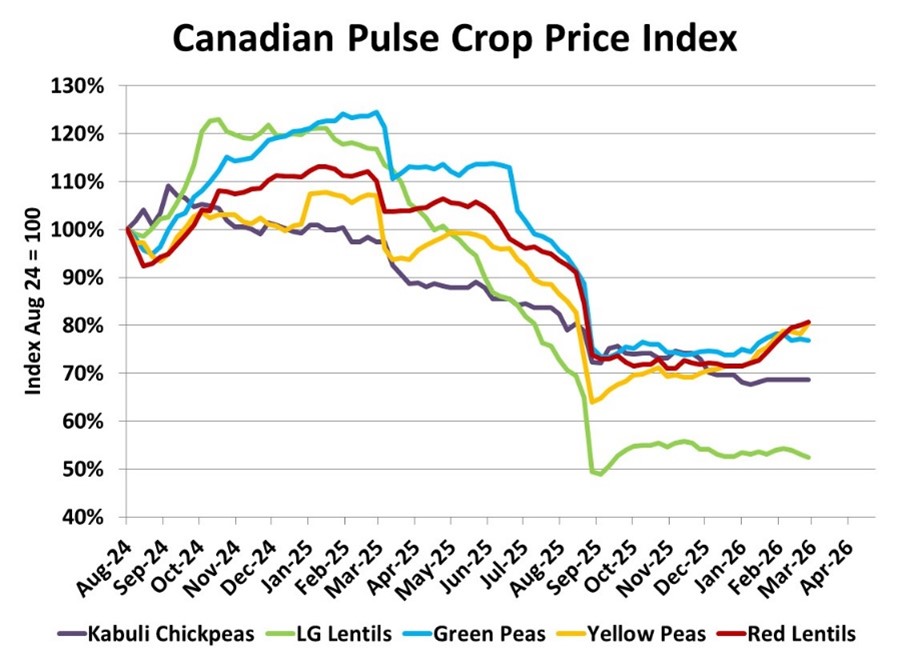

The most noteworthy event was the announcement by the Chinese government to scale back or eliminate import tariffs on canola seed, canola meal and peas, which injected more optimism into those markets. This development added some support for prices which could, in turn, shift a few more acres in that direction. Prices for other crops like barley, wheat and red lentils are moving higher seasonally, which could also make those look a bit more attractive.

For the most part though, StatsCan’s estimates a pulse crop acreage seem to be within reason. Seeded area of peas was reported at 3.08 mln acres, 12% less than last year and in line with the average trade guess. Both yellow and green pea prices are lower than a year ago, but the decline is sharper for green peas, which could discourage a few more of those acres. But as mentioned above, more certainty with respect to exports to China could bring a few more peas, particularly yellows, back into rotations.

Fewer acres of peas along with a return to an average yield would mean the 2026 crop could shrink by over a million tonnes. This should help ease the heavy supply situation to some degree but wouldn’t make things “tight”. The old-crop carryover from 2025/26 is expected to be historically large and offset much of a reduction in the 2026 crop.

StatsCan also showed a decline in 2026 lentil acreage, although not to the same extent as peas. Seeded area was reported at 4.14 mln acres, 5.5% lower than last year but above the average trade guess of 3.9 mln acres. This reduction would be fairly modest and leave lentil acreage in line with the 5-year average. While StatsCan doesn’t provide a breakdown by type in this report, we would expect a shift to red lentils, back to a more typical two-thirds share of acreage. This would mean a larger cut in green lentil acres, which the market definitely needs.

Just like peas, fewer lentil acres and a drop back to the average yield would mean a large decline in the size of the 2026 crop, a step in the right direction for a heavily-supplied market. That said, most of that production loss would be offset by the large old-crop carryover from 2025/26, with an emphasis on green lentil supplies.

Chickpeas are the exception in StatsCan’s lower estimates of pulse acreage. Seeded area is forecast at 575,000 acres, 6% more than last year. Even with more acres, a drop back to the average yield would mean a noticeably smaller crop in 2026. But the recurring theme of heavy supplies will also limit the impact of a smaller chickpea crop, with the very large old-crop carryover from 2025/26 resulting in even larger supplies next year. Export demand has been strong for chickpeas, but that may not be enough to keep supplies from feeling heavy again in 2026/27.

StatsCan’s estimate of dry bean acres was a bit puzzling, showing a 31% drop at 295,000 acres. That would be the lowest total since 2015. While prices for pinto and black beans are currently low, we’re skeptical that seeded area will decline that much, partly because StatsCan’s coverage of dry beans has been “patchy” in the past. Seeded area will likely be lower, but not by that much.

Pulse Market Insight provides market commentary from Chuck Penner of LeftField Commodity Research to help with pulse marketing decisions.