Are US Acreage Changes a Signal for Canada?

A few weeks ago, StatsCan released its seeding intentions estimates for 2026, but these were the results from a very early farmer survey. This raised lots of questions about whether farmers have changed some planting decisions since then. This past week, the USDA issued its own set of 2026 acreage forecasts, but these survey results were more current by a couple of months.

Farmers on both sides of the border generally see the same kind of price signals and cropping practices aren’t all that different. As a result, we wonder whether the more recent USDA estimates could provide a few fresh clues about acreage changes in western Canada.

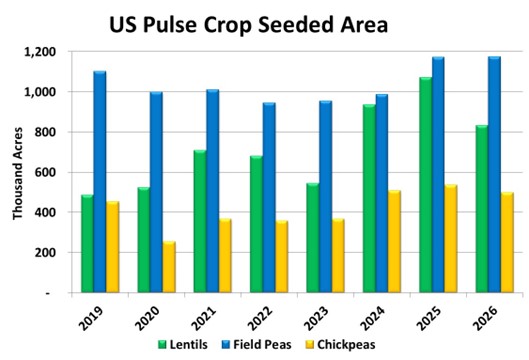

In its estimates, the USDA is forecasting seeded area of peas at 1.17 mln acres, almost identical to 2025, and this would be the second highest total ever. This is a bit surprising, given that US pea exports have lagged in 2025/26 and prices there haven’t benefited from Chinese buying, like Canadian peas have.

Earlier, StatsCan forecast a 12% decline in Canadian pea acreage but again, this was based on a farmer survey conducted before China dropped its import tariffs. It’s quite possible that the Canadian acreage number will be revised higher and if it matches the 2025 total, the 2026/27 supply outlook could be more comfortable than expected earlier.

The USDA reported a much larger change for 2026 lentil acres, with a 22% drop in seeded area at 832,000 acres. That shouldn’t be all that surprising as 2025 acreage was a near record and a return to more typical levels could be expected. More importantly, a large portion of US lentils are green varieties (mainly medium greens), and those prices have seen large price declines, discouraging more acres.

In western Canada, StatsCan estimated a more moderate 5.5% decline in lentil acreage. But looking beneath the surface, seeded area of green lentils will almost certainly drop more sharply, which could mirror the US declines. At the same time, red lentil acreage in western Canada will likely see an increase.

Seeded area of chickpeas in the US is forecast to drop by 7% in 2026. That’s the opposite direction from StatsCan’s estimate of a 6% increase. If 2026 chickpea acreage remains fairly steady on both sides of the border, that wouldn’t be too surprising. That said, these changes are relatively minor and we don’t want to read too much into them, especially since both the USDA and StatsCan have made sizable revisions to their chickpea estimates in recent years.

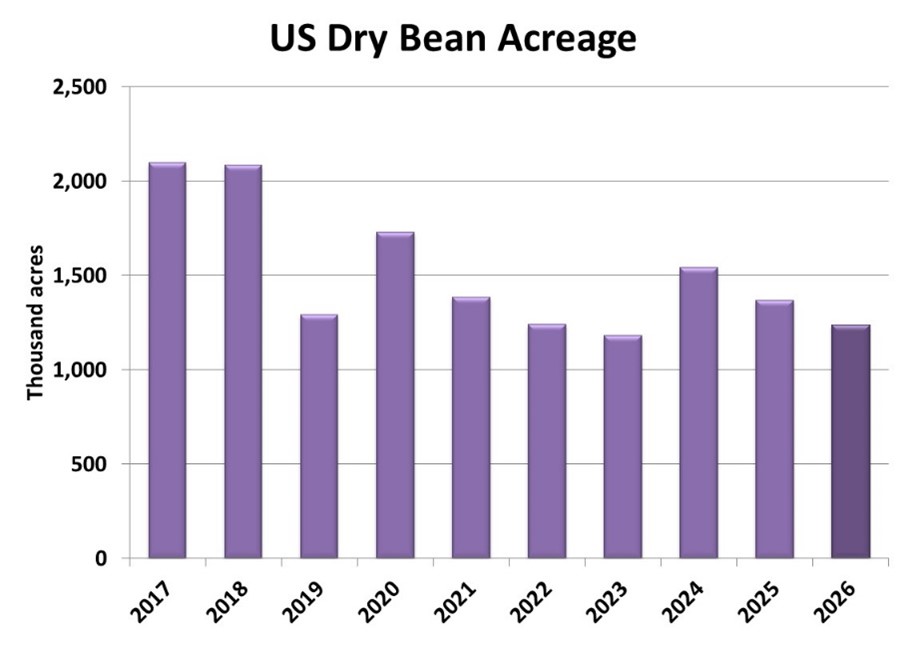

The USDA pulse estimate that could be the strongest clue about Canadian acreage is for dry beans, which are forecast to decline 10% from last year. StatsCan’s dry bean acreage estimates were incomplete for several provinces, and those gaps made it difficult to get a good handle on Canadian acreage. If seeded area on both sides of the border declines by 10%, lower North American supplies could make the 2026/27 market a bit more interesting.

Of course, these are only acreage numbers. The main ingredient in the supply outlook is yield. At this point, we think in terms of average yields, and there’s no way to make an accurate forecast until well into the growing season.

Pulse Market Insight provides market commentary from Chuck Penner of LeftField Commodity Research to help with pulse marketing decisions.