Third Quarter Scorecard Positive for Pulses

More acreage and very high yields meant much bigger Canadian pulse crops in 2025. Pea and lentil crops were each nearly 1.0 mln tonnes larger than 2024 and chickpea production was up by almost 200,000 tonnes. And for each crop, the carryover from 2024/25 into 2025/26 was also large, which added to the big supplies.

With pulse crops facing extremely heavy supplies, a serious increase in export volumes was needed in 2025/26 to keep markets from being pressured (even) lower. And early in the marketing year, prospects weren’t great. In fact, the most positive developments only started to show up in the third quarter of the 2025/26 marketing year. While that doesn’t leave a lot of time to “fix” the heavy supply situation, the outlook is certainly brighter than it was a few months ago.

Prospects were especially dim for peas earlier in 2025/26, with Chinese tariffs essentially shutting off that important outlet for Canadian peas. Indian demand was mediocre but other countries stepped up and kept pea exports flowing at a decent pace. Of course, the big pea supplies meant “decent” exports weren’t enough. Fortunately, China announced in January that it was dropping its tariffs, triggering a sharp improvement in exports by late February.

The chart above only shows bulk pea (mostly yellow) exports reported by the CGC but it clearly demonstrates how things have changed. As of week 39, the end of the third quarter, bulk pea exports reached 2.08 mln tonnes compared to 1.58 mln tonnes in 2024/25. Even if the pace moderates in the final quarter, Canadian exports will remain strong, the most since 2020/21. That means 2025/26 pea ending stocks will be large but not massive, which was certainly a concern earlier in the year.

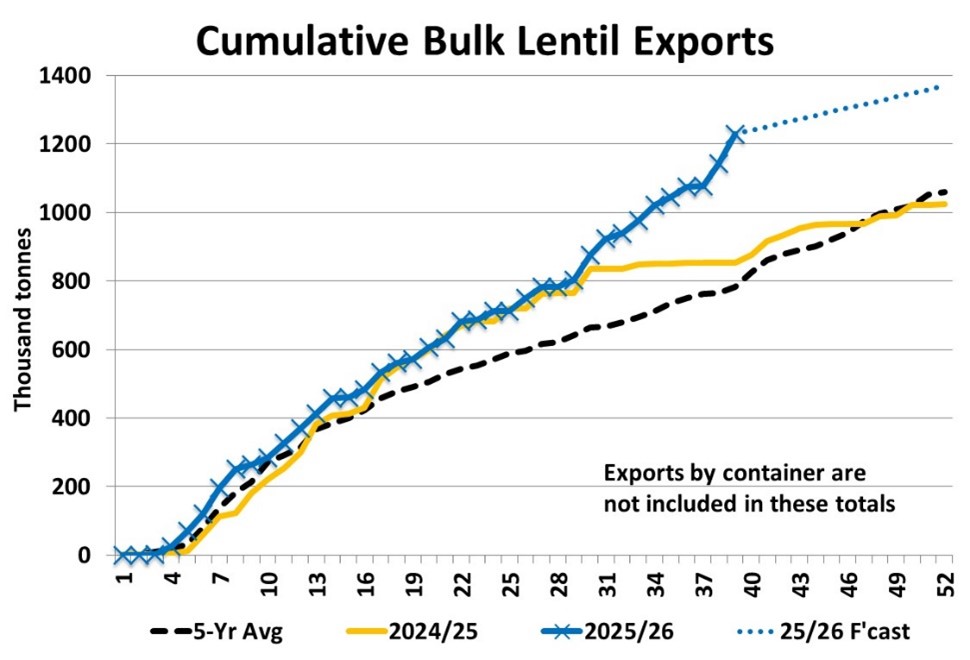

The chart below shows the CGC data for bulk lentil exports, which would largely be red lentils. Exports were good through the first half of 2025/26, keeping pace with the previous year and well above average. That said, to offset the big increase in the 2025 crop, exports needed to be more than “good”; great exports where necessary. Fortunately, the pace of exports turned strongly higher starting in late February, in sharp contrast to the 2024/25 slowdown.

By the end of the third quarter of 2025/26, bulk lentil exports reached 1.23 mln tonnes versus the average of 0.78 mln tonnes. Even if exports slow in the fourth quarter, as they sometimes do, the full-year total should be the most since 2020/21. That’s good news for the red lentil market as those ending stocks will be reasonably large but not massive, and better than expected earlier this year. The CGC export numbers don’t reflect green lentil exports but the StatsCan data to the end of March shows above-average volumes of green lentil exports. Unfortunately, that pace isn’t nearly enough to draw down the huge stockpile of Canadian green lentils, so the heavy supplies will continue.

Among the pulses, chickpeas are showing the best export performance in 2025/26, with a record pace. The CGC doesn’t report chickpea exports, as those are all done by truck to the US or by container but StatsCan’s exports to the end of March are 168,000 tonnes, far ahead of the average of 121,000 tonnes. While that’s very positive, there are still lots of chickpeas, including low quality, still on farms. But the trend is in the right direction. That hasn’t been enough to lift chickpea prices but has at least kept him stable.

Pulse Market Insight provides market commentary from Chuck Penner of LeftField Commodity Research to help with pulse marketing decisions.