Fewer Pulse Acres Add a New Twist to a Soggy Season

Leading up to StatsCan’s June acreage estimates, we thought there could be a few surprises in the numbers. There were, and for pulse markets, most of them landed on the friendly side. The survey showed fewer pulse acres than last year across the board and, in most cases, fewer than StatsCan’s March intentions. Layer on the excess moisture still hanging over large parts of the prairies and the supply picture for 2026/27 is starting to tighten in a hurry.

Peas provided the biggest surprise. Instead of the small bump in acreage some were expecting, StatsCan reported 2026 seeded area at 3.03 million acres, 14% less than last year and a bit below its March forecast. The breakdown by type was even more interesting. It would have been reasonable to expect green and minor classes to lose the most ground after their relatively weak price performance, but yellow pea area actually took the biggest hit, down 16% at 2.31 million acres, while green pea acres slipped 10% and “other” classes were up slightly.

The implications are mostly about yellow peas. A considerably smaller crop would actually force export volumes to be rationed at the same time as demand from China and India is expected to strengthen. That kind of squeeze tends to produce a sharper price response, and it gives yellow peas considerable upside potential for 2026/27, with green pea supplies still comfortable enough to keep that market on a steadier path.

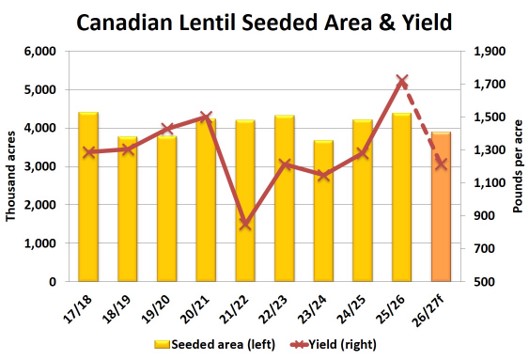

The lentil story rhymes with peas, with one important difference by type. Total lentil area came in at 3.90 million acres, down 11% from last year and below the March forecast. Red lentil acres actually increased 14% to 2.44 million acres, returning to a more normal share of total lentil area, while the reductions were concentrated in the green classes: large greens down about a quarter, small greens down more than half, and other minor classes down about 30%.

Hanging over all these numbers is the moisture situation. Soil moisture across large parts of the pea and lentil growing areas is running well above normal, and pulses are more vulnerable than most crops to wet feet, with root rot and other diseases thriving in these conditions. To be clear, plenty of areas still look very good and it will take time before the damage elsewhere can be measured. But yield estimates are now tilted to the downside, with implications for both quantity and quality.

The same StatsCan report trimmed chickpea and dry bean acres too. Chickpea area was marginally below last year, but the market is still working through a very large old-crop carryover, so total supplies will stay comfortable and the price response should be muted. Dry bean area dropped 21%, with coloured bean classes down about 30% while white bean acres were slightly higher. Combined with the smallest US dry bean area in decades, that sets the stage for firmer new-crop bean bids, especially for blacks and pintos.

Pulse prices in western Canada haven’t yet responded to any of this, with old-crop and new-crop bids still drifting sideways to lower in line with their usual seasonal patterns. But the ingredients for a firmer market are stacking up: fewer acres, genuine yield risk and demand question marks that lean friendly. For growers who can manage the risk, patience on further new-crop sales remains a sensible stance. Prices typically recover once harvest gets underway, and this year’s fundamentals suggest the rebound could come with some extra force, particularly for yellow peas and red lentils.

Pulse Market Insight provides market commentary from Chuck Penner of LeftField Commodity Research to help with pulse marketing decisions.