What to Watch for in 2019

Pulse markets have endured some significant turbulence in 2018, with farmers and traders having to deal with large risks. And that’s not even taking the weather into account. It goes without saying that each year brings its own set of challenges. There’s simply no way to know all of the good, bad or ugly things that will happen in 2019 and it’s probably better that way. But there are some things to watch for already that will influence old-crop and new-crop pulse markets.

As always, India tops the list of influences for pea and lentil markets. Currently, import barriers are still in place, with tariffs on peas and lentils, quantitative restrictions (although a little leaky) on pea imports and extra costs related to fumigation. These barriers were all put in place because of heavy supplies of pulses from record domestic crops and large imports.

There’s been a lot of talk about how India’s next election in April or May could be the catalyst of a change in its import policies, but that’s unlikely to change things. If the current government is re-elected, it still won’t want to anger farmers by opening up the borders to pulse imports. Opposition parties are building their strength based on farmers’ anger and would be reluctant to lower import barriers.

As always, weather will have the final say and there are stronger signals that India’s rabi crop will be smaller than last year’s record, and possibly well below average. Seeded area of rabi (winter) pulses is down 9% from last year and 2% below average. The moisture situation is more serious. Even with some rainfall in eastern India in the past week, the core production regions in central and northern India are very dry. Rainfall at the end of the kharif (summer) season that usually provides a moisture reserve was well below normal and so far in the rabi season, precipitation has been less than 20% of normal.

If this situation doesn’t improve quickly, Indian crops of chickpeas, peas and lentils will be sharply reduced and this will force the government to open the borders to imports as domestic prices start to rise. This might still not occur until after the next election, so it wouldn’t be a quick fix. Even so, there’s a lot more optimism in pulse markets than there has been for at least the year.

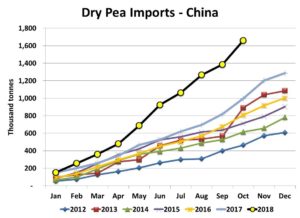

The other key market we’re watching, especially for peas, is China. There are a couple of concerns regarding Chinese trade, with the most recent being the diplomatic tensions between Canada and China. Actions that China might take arising from this situation are a concern, but are largely unpredictable.

The other question related to China is whether the resumption of soybean imports from the US could dampen demand for Canadian peas in its feed market. While there could be slightly reduced demand for peas by Chinese buyers, it’s worth noting that pea demand has been rising year-over-year, which suggests that even if feed use in China is cut back, overall demand will remain strong.

Of course, there’s the outlook for the Canadian pea crop in 2019/20. With bids for both green and yellow peas firming up the last couple of months, we expect this will provide more optimism for Canadian farmers. Likely, this will cause an increase in plantings this spring. Our current forecast for 2019 pea acreage is 4.0 mln acres, 10% more than 2018 but (with average yields) that’s not expected to be enough to weigh heavily on the market.

Lentil acreage could also edge higher due to the recent upturn in lentil bids. Even though prices are nowhere close to the market highs, this bit of optimism will likely add to 2019 acreage. Our forecast for a small 3.5% acreage increase won’t be enough to weigh too much on the market, as long as yields are close to average.

Overall, we’re fairly optimistic about the outlook for the 2019/20 pea and lentil markets. All indications seem to be pointing toward the market turning the corner and prospects improving.

Pulse Market Insight provides market commentary from Chuck Penner of LeftField Commodity Research to help with pulse marketing decisions.