StatsCan Acreage Numbers Just the Start

This week, StatsCan issued its estimates of 2022 seeded area for Canadian crops. The numbers are based on a survey of 25,000 farmers from May 13 to June 12. Yes, there are always questions about the numbers, especially once they’re sliced and diced for smaller crop types, but they are still the best starting point when looking at crop potential.

In spite of historically strong prices for all pulses, a couple of crops experienced sizable declines in 2022 seeded area, a clear sign of this year’s intense acreage competition. Just as important though, most changes from StatsCan’s April acreage forecast were fairly small and not far from expectations.

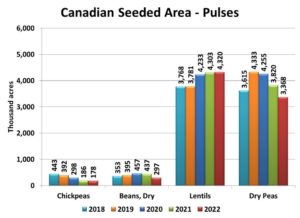

Seeded area of peas was reported at 3.37 mln acres, down 12% (450,000 acres) from last year. Because of planting delays this spring, there were reports that a lot more pea acres were getting dropped. It’s possible these late changes weren’t caught in the StatsCan survey and the final numbers might be a bit lower yet. StatsCan showed similar declines for both green and yellow peas, a bit of a surprise (to us).

Of course, pea yields can offset the loss of acres, especially after last year’s disastrous crop. In fact, the 2022 pea crop will certainly be bigger than 2021. We can try numerous yield scenarios but all of them would be high enough to produce a solid crop recovery. For example, using the pre-2021 average yield of 38.9 bu/acre would result in a 3.5 mln tonne pea crop, 55% more than last year. Even if it’s a bit lower though, it doesn’t really change the outlook. Keep in mind, a 3.5 mln tonne crop is well below the pre-2021 average of 4.3 mln tonnes.

Lentil seeded area was pegged at 4.32 mln acres, basically unchanged from last year but 4% less than StatsCan’s April number. We’ve heard differing opinions (in both directions) about lentil plantings, so unchanged could be about right. In the breakdown by type, there were only small shifts between reds and greens.

Just like peas, the big change for the Canadian lentil crop won’t come from the acreage numbers, but rather the yield. Conditions in early July are far better than last year although damage to the 2022 crop is still possible (more likely from too much moisture than not enough). If we would plug in the pre-2021 average yield of 1,360 lb/acre (22.7 bushels), the 2022 lentil crop would end up at 2.6 mln tonnes, a full million more than 2021 and in line with the average crop prior to 2021.

StatsCan’s seeded area number for chickpeas at 178,000 acres was nearly unchanged, both compared to last year and its April estimate. As a result, the only change in the 2022 crop will be the result of a different yield. There are still some trouble spots, but a repeat of 2021 is not in the cards. A return to the pre-2021 average yield of 1,570 lb/acre would mean a crop of 120-125,000 tonnes. That would be a 60% increase over last year but still smaller than crops prior to 2021.

StatsCan showed a large 32% drop in dry bean plantings, now just below 300,000 acres. The largest declines showed up in western Canada, partly because of planting delays, but bean acres were also down in Ontario. Because the crop is spread across the country, the 2021 drought had less impact and a yield recovery in 2022 won’t be enough to offset the drop in acres. The 2022 crop will be smaller.

Seeded area of fababeans was also reduced to 72,000 acres, 46% less than last year. That said, a rebound in the 2022 yield could essentially offset the fewer acres, leaving the crop size similar to last year’s 75,000 tonnes.

Pulse Market Insight provides market commentary from Chuck Penner of LeftField Commodity Research to help with pulse marketing decisions.