Pulses Avoiding the Volatility of Major Markets

This is the time of year when crop markets are transitioning from old-crop to new-crop dynamics. In years when supplies are well-balanced and prices are close to average, those transitions are usually minor. But 2021/22 has been anything but normal with tight supplies and extreme prices. So it’s hardly surprising that the shift to new-crop markets has been “exciting”, at least for some crops.

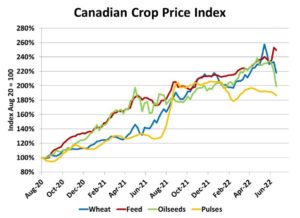

For better or worse, crops traded on futures exchanges like canola and wheat are affected by speculative activity. Sometimes that drives prices higher than they would otherwise, but the opposite is also true, causing the sharp sell-offs lately. This also increases the odds that markets will overreact with the big swings and corrections we’re seeing in this transition to 2022/23.

These new-crop transitions also affect pulse markets and other cash-traded crops. The difference is that speculators don’t exaggerate the moves. Pulse prices have been historically strong in 2021/22 but didn’t see the extreme spikes in some other crops. But that’s also one reason why pulse prices haven’t dropped nearly as hard as canola or wheat have recently.

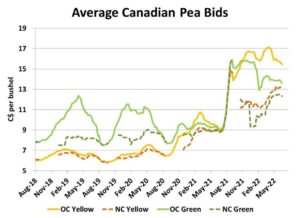

Prices for pulses are already shifting toward new-crop price levels but the moves will likely be milder. Part of the reason is that the difference between old crop prices and new-crop bids are fairly narrow, so there’s less room for them to drop.

It won’t just be old-crop prices changing though; new-crop bids will also respond as the crop develops and matures over the next few weeks. There are still trouble spots in various parts of the prairies but overall, the worries about dryness have been fading. In fact, excess moisture is already starting to become a concern, particularly for pulses.

Despite these issues, it’s hard to imagine 2022 crops could be as small as last year. Even with the challenges, production and supplies will almost certainly improve and if that’s the case, it makes sense that prices in 2022/23 will be lower than the highs of 2021/22. It’s not whether the 2022 crop will be bigger, but how much bigger. As those outlooks get clearer, new-crop prices will start to adjust too.

On one side of the trade, overseas buyers will be sorting out how aggressively they should be bidding for the 2022 crop. Last year, some waited too long to lock in supplies and had to pay even higher prices after harvest. This year, they’re nervous about locking in supplies at current prices if a bigger crop will be available. As a result, there hasn’t been a whole lot of buying just yet.

From the farmer’s perspective, forward-contracting the 2022 crop has been very limited, for good reasons. A lot of hard lessons were learned last year when contracts couldn’t be filled or those early contracts were at the lowest prices of the season. The extreme dryness this spring added even more caution. Thus, it’s completely understandable that very little of the 2022 crop has been priced so far.

Eventually though, both buyers and sellers will need to step up, and that’s going to cause markets to adjust. As farmers are more confident that they’ll have a decent 2022 crop, selling is going to kick into gear. Last year, farmers reluctance (or inability) to sell gave the market more support, but with larger supplies, it will be harder to keep prices elevated.

Buyers too will need to get in the game, with the fall shipping season not too far off. When they do, they’ll need to keep their bids aggressive to convince farmers to sell their 2022 crop. The timing of who “blinks” first could be an important piece in how the to new-crop transition unfolds.

Pulse Market Insight provides market commentary from Chuck Penner of LeftField Commodity Research to help with pulse marketing decisions.