Updated StatsCan Acreage Eye-Opening

Amid all the other uncertainty about pulse crops in 2025, we now have bit more clarity about seeded area. StatsCan has released updated acreage numbers based on a large survey of farmers and although its estimates are always debatable, they provide a good starting point.

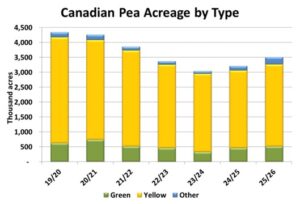

StatsCan estimated 2025 seeded area of peas at 3.50 mln acres, up 9% from last year and the most since 2021/22. Clearly, farmers weren’t scared off by Chinese import tariffs and the prospect (at the time of seeding) of tariffs by India. Green pea area rose to 520,000 acres, 12% more than last year, and yellow pea area expanded to 2.74 mln acres, up 6% from the previous year. The biggest percentage change showed up in the “other” category, which includes maple peas. Seeded area of minor classes was reported at 240,000 acres, 55% more than last year and a new record.

While yields are far from certain, the increased pea acreage has the potential to cause supplies to expand for 2025/26. Larger old-crop carryover and a bigger 2025 crop would mean sizable supplies, which means next year’s export outlook becomes even more important. If exports to China and India are reduced, 2025/26 ending stocks could end up very large.

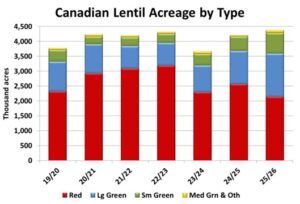

For lentils, StatsCan added 200,000 acres to its earlier estimate, with seeded area now at 4.38 mln acres, 4% more than last year. That wasn’t really a surprise, but the breakdown by type was much more interesting. According to StatsCan, seeded area of red lentils dropped to 2.15 mln acres, 16% less than last year and the lowest since 2018/19. At the same time, seeded area of green lentils hit 2.23 mln acres, 36% more than last year.

The big increase for green lentil area raises the potential for overproduction, which seems to be the main driver of lower prices in the last few months. Of course, the crop is far from being in the bin and the main growing areas for green lentils are once again the driest parts of the prairies. Even though conditions might be a bit better in red lentil areas, the drop in acreage will mean a smaller crop in 2025.

StatsCan reversed course for chickpea plantings, from a decline in its March estimate to a sizable 13% increase in late June. The total area of 541,000 acres is the most since way back in 2001/02 and even if yields are reduced this year, 2025 production will be up and supplies will be very comfortable.

Seeded area of dry beans was also bumped up from StatsCan’s March estimates but still lower than last year. StatsCan reported 382,000 acres of dry beans, 5% less than a year ago, with gains in white bean acreage while coloured bean area was reduced. Fababean area was reported down 15% at 69,000 acres.

Of course, yield prospects are still very uncertain. Sizable parts of the southern prairies, especially where green lentils and chickpeas are grown, are most vulnerable. Key growing regions for peas started off poorly but some (not all) are looking a bit better. At the same time, hot dry conditions are kicking in during key flowering and podding stages. Acreage is just one part of the picture, with the yield portion still to be determined.

Pulse Market Insight provides market commentary from Chuck Penner of LeftField Commodity Research to help with pulse marketing decisions.