Weather Market or Not?

There’s no shortage of question marks about 2025 crop production. StatsCan will issue updated acreage numbers on June 27 and the USDA will release its latest acreage estimates on June 30. These reports should provide some direction for the 2025/26 crop outlooks. It will be interesting to see whether all the trade uncertainty caused farmers to shift acreage, including for pulses. But that’s just the beginning of the story.

We’re still just in the first month of the growing season and already, it’s been a roller coaster in many parts of the prairies, in some ways similar to 2024. Prior to seeding in late March, there were a few dry areas on the prairies but overall, conditions seemed positive and there was some early optimism. Move forward to the end of April though and the AAFC Drought Monitor map showed expanding areas of drought, particularly in the northern prairies, where pea acreage is concentrated. By the end of May, the drought situation had spread across most of the prairies, with the most serious shortfalls in northern Saskatchewan and the Peace River region.

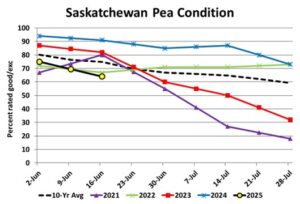

The dryness in the northern half of the prairies caused a poor start for the 2025 pea crop in Saskatchewan. According to Sask Ag, the crop rating for peas at the beginning of June was 75% good or excellent. On the surface, that doesn’t sound too bad, but it was worse than the 10-year average of 80% and far below last year’s starting point of 94% good/exc. Fast-forward two weeks and the mid-June ratings worsened, dropping to 64% good/exc versus the 10-year average of 75%. So far, crop ratings aren’t available from Alberta but based on rainfall and soil moisture maps, we expect conditions there to be a bit better than Saskatchewan.

For lentils, conditions started the 2025 growing season a bit better than peas. Largely, that’s because earlier this spring, it wasn’t quite as dry where most lentils are grown in the southern half of the prairies, at least as compared to the north. At the beginning of June, 79% of Saskatchewan lentils were rated good or excellent, a bit better than the 10-year average of 77% but still trailing last year at 96% good/exc. Since then though, there’s been a noticeable drop as the southern prairies dried out. In mid-June, the crop ratings dropped to 60% good/exc, the lowest mid-June score since 2019 (which improved later in the year).

So far, these deteriorating conditions haven’t caused any price reaction for either old-crop or new-crop pea or lentil bids. Those have mostly been steady to lower in recent weeks. This isn’t unusual as it fits with the normal seasonal tendency when overseas buyers wait for fresh supplies from the upcoming harvest. Even in the epic 2021 drought, bids for peas and lentils slipped lower seasonally in the early summer. That weakness in 2021 was short-lived though, only lasting until early July before turning strongly higher.

The other reason for the lack of price response is that prairie weather in the last week has become more unsettled and forecasts have turned optimistic for many parts of the prairies. While the worst hit areas are already facing losses, there is potential for recovery in other places. There are no guarantees with the forecasts, but it’s simply too early to write off the crop in most parts of the prairies.

At this point, 2025 crops could pivot in either direction. At the risk of stating the blinding obvious, a return to hot dry conditions would do serious damage and boost prices, although that reaction would likely be delayed. At the same time, if the latest forecasts pan out and an unsettled weather pattern continues, prices will continue to run lower seasonally in the short-term. The good news is that prices usually start to recover shortly after harvest regardless, even if crops turn out well.

Pulse Market Insight provides market commentary from Chuck Penner of LeftField Commodity Research to help with pulse marketing decisions.