Big Supplies Mean Patience and Modest Expectations Needed

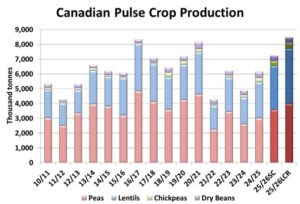

Not everyone had impressive pulse yields this year but there were enough positive results that big crops and big supplies are a key feature in the 2025/26 outlook. According to StatsCan’s September estimates, total pulse production this summer was just over 7.2 mln tonnes, over a million tonnes more than last year and the most since 2020/21.

Other sources indicate yields were a lot bigger than StatsCan. Most feedback we received during harvest pointed to yields well above average and provincial crop reports seem to back up those claims. For example, pea yields reported by Alberta Ag and Sask Ag were both 6-7 bushels per acre higher than StatsCan’s estimates for those provinces. Likewise, the lentil yield from Sask Ag was 32.0 bu/acre versus StatsCan at 24.4.

If we plug in these higher yield estimates, the 2025 pulse crop moves from “large” to “record large”, rivaling production of 2016/17. Not each crop would be a record in 2025. In fact, only lentils would be the largest crop ever but total pulse production would be just shy of 8.5 mln tonnes, up 2.3 mln tonnes (38%) from last year.

If demand is strong enough, big pulse crops don’t have to mean extremely low prices, but they certainly don’t help. And it would be nice if the regular laws of supply and demand wouldn’t apply this year, especially for those who didn’t get the big yields this summer, but they do.

Western Canadian bids for peas and lentils since 2010/11 are shown in the chart below. Prices don’t always respond directly to the size of the crop, at least not every year. For example, pulse prices generally strengthened in 2020/21 even though production was close to a new record. That said, the gains that year were fairly modest, especially compared to the spike caused by the drought in 2021/22.

Most times though, markets responded as expected with bigger production resulting in weaker prices. The large pulse crop in 2016/17 triggered a drop in prices, and the market (aside from green peas) took several years to recover.

Pulse prices this fall have reacted according to the laws of supply and demand, but this year’s declines seem to be much more severe. That’s especially the case for green peas and green lentils, which had been historically high and had further to fall.

If prices would reverse course and strengthen in the face of record supplies, demand would need to pick up in a big way, and soon. Unfortunately, the outlook for increased export business is cloudy, at best. Canadian peas are still facing 100% import tariffs from China and although trade talks are ongoing, the odds of a resolution are still fairly low. Another big concern is India, Canada’s other major pulse buyer. Rumours are still circulating about the potential for increased import tariffs but even if that doesn’t happen, Indian buying has been quiet.

In this type of environment with big crops and limited demand, it will take longer than usual to clear the market of the large supplies. This means a fair amount of patience will be needed and price expectations should be limited, looking for opportunities to make small gains during the year rather than waiting for a major rally.

Pulse Market Insight provides market commentary from Chuck Penner of LeftField Commodity Research to help with pulse marketing decisions.