Western Canadian Weather Roller Coaster Adds Uncertainty

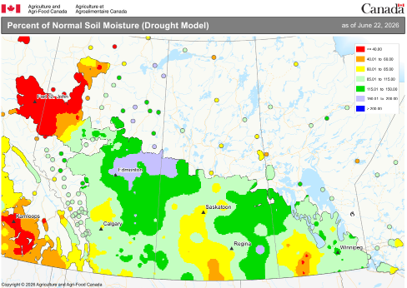

It’s not even the end of June, but the weather in western Canada has already experienced more twists and turns in 2026 than in recent memory, with the biggest changes occurring in the western prairies. It was only a month ago that soil moisture maps for Alberta looked mostly orange and red and there were widespread concerns about possible drought. Now, the moisture maps for Alberta are mainly green and blue, a very quick turnaround.

Various reports from numerous locations show a wide range of crop conditions as of late June. We’re hearing that large parts of Alberta, mostly in central and southern regions, are looking quite positive. Other areas, particularly in the western and northern Peace River region, are still dry. At the other end of the spectrum, reports from northeast and northwest Alberta are telling us about standing water and flooded crops. Other parts of the prairies are experiencing very variable conditions, from “great” to “ugly”.

Most often in western Canada, the biggest problems facing the crop are caused by dry conditions but so far in 2026, the opposite is true. And with more rain on the way, areas that are already too wet won’t be seeing any relief and it may get worse. Which brings us to pulse crops.

Excess moisture is a big problem for all crops, reducing yields and lowering quality, but pulses are even more susceptible to wet conditions and high humidity. Root rot and other diseases flourish under these conditions and have been serious issues in the past, taking their toll on pea, lentil and chickpea crops.

Of course, it’s too soon to make any reliable crop forecasts, either in terms of acreage or yields. StatsCan will release its updated acreage estimates at the end of June, based on a farmer survey, and there could be a few surprises in those numbers that affect crop size. Keep in mind though, planting delays in Saskatchewan and drowned-out low spots in Alberta will trim a few acres from the total. Yields are another question entirely. Last year’s exceptionally high yields will be difficult to repeat, especially if conditions remain wet.

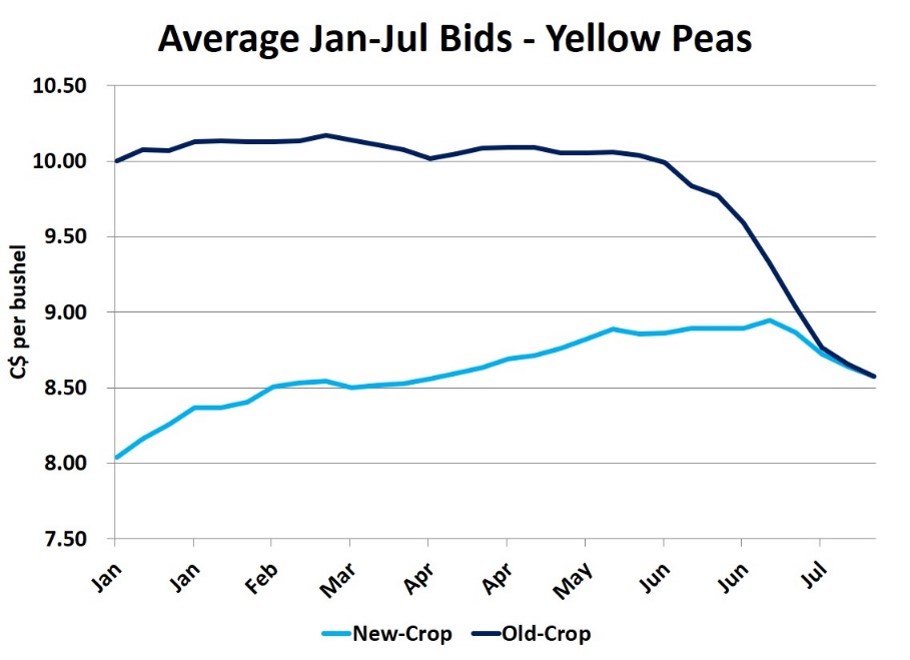

This uncertainty about acres and yields could keep farmers on the marketing sidelines, especially those in areas where conditions are the wettest and the crop outlook is the diciest. Even though forward pricing is an effective risk management practice, holding back on further sales could be a solid marketing decision at this stage of the year. Besides the risk of lower production, historical patterns show that patience could be rewarded. Old-crop bids for yellow peas normally start declining in early June and new-crop bids turn down toward the end of the month. A similar pattern applies for green peas, red lentils and green lentils.

What this chart doesn’t show is that once the harvest is underway, pulse prices tend to start recovering. The size and speed of the rebound varies from year to year, depending on the outcome of Canadian crops, but also due to factors affecting demand. For 2026/27, the precarious situation in India could be the linchpin for pulse markets. With the uncertainties surrounding Canadian pulse crops, including the risk from excess moisture, and concerns about Indian pulse production, waiting on the sidelines to make sales for this year’s crop could turn into a wise choice.

Pulse Market Insight provides market commentary from Chuck Penner of LeftField Commodity Research to help with pulse marketing decisions.