StatsCan Production Numbers Leave Questions

Call me old-fashioned, but I’m really missing the way StatsCan used to gather crop yield information by phoning farmers. Maybe I’m more nostalgic because I wasn’t the one getting interrupted while I’m working or eating supper, but it seems we’ve really lost a solid benchmark without the boots-on-the-ground estimates.

Over the past few years, StatsCan has “evolved” in its yield estimation processes. A few years ago, it changed its September yield estimate to a model-based system using satellite vegetation images, but that September estimate still had a benchmark of an early farmer survey conducted around the end of July to get early yield estimates (and July 31 on-farm stocks). The two different sources could then be compared against each other to improve reliability.

This year, StatsCan shifted to using satellite images for both its August and September yield and production estimates, without any farmer-level verification or comparison. For pulses (and other crops), this model-based approach leaves a lot of questions, since we know yields are based on more than just the colour and density of the crop canopy.

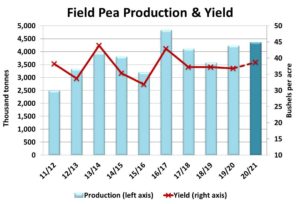

From the first to the second StatsCan production estimates, the 2020 pea crop dropped from a record of 5.0 mln tonnes to 4.4 mln tonnes, a big decline but it seems much more reasonable. This latest estimate would be up slightly from last year but, with a smaller carry-over from last year, total 2020/21 supplies would be very close to the same as last year.

The steady supplies mean that if prices are going to behave differently in 2020/21, it would depend on changes to the demand side of the equation. In general, we expect strong exports again to China and some countries in South Asia bordering on India. There should also be an increase in Canadian domestic processing in 2020/21 as new fractionation plants come on stream.

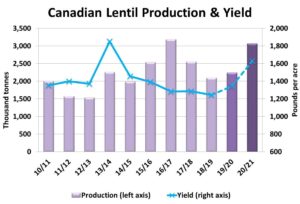

The StatsCan production estimate for lentils did the opposite of peas, rising from 2.8 mln tonnes in its first estimate to 3.1 mln, the second largest crop on record. On the surface, this increase suggests 2020/21 supplies will get extremely heavy but because of the surge in exports late in 2019/20, the carry-over from 2019/20 was extremely low and will mostly offset the bigger 2020 crop. And we’re not quite convinced the yields are actually as high as reported by StatsCan anyway.

Again, the 2020/21 supply outlook seems like it could be quite heavy but there are also plenty of signals that demand will also be very strong in the coming year. If that’s the case, this big lentil crop could get chewed through fairly easily and the market would remain well supported.

StatsCan also raised its estimate of the chickpea crop. Earlier it looked like the crop would be down sharply from last year but now it’s only slightly lower at 239,000 tonnes. The problem for the chickpea market is that StatsCan is also indicating extremely large carry-over of old crop supplies, making 2020/21 supplies very burdensome.

The 2020 dry bean crop from StatsCan was also larger in its second set of estimates, but there were virtually no old-crop dry beans left at the end of 2019/20. As a result, the increase in dry bean production should be able to find a home in export markets fairly easily. Even so, there was a sizable transition from sky-high prices at the end of 2019/20 to more typical prices in 2020/21.

Pulse Market Insight provides market commentary from Chuck Penner of LeftField Commodity Research to help with pulse marketing decisions.