Changes to StatsCan Process Leave Acreage Questions

Several years ago, StatsCan started responding to feedback about farmers’ “survey fatigue”. StatsCan shifted its August and September yield reports away from farmer surveys and used satellite vegetation images and computer models. Now, StatsCan has decided that asking about farmers’ seeding intentions in spring could be rolled into an existing survey that’s done in mid-December to mid-January.

Some parts of farmers’ crop rotations and acreage were already decided by mid-winter, but certainly not all, as the 2022/23 marketing year wasn’t even half over. Crop insurance coverage rates hadn’t been announced and for some crops, new-crop bids weren’t even available yet. Markets still had a lot of time to change and price relationships for the various crops were still evolving.

Some people might think this is just some whining from market analysts. My response is that reliable estimates are important for all market players, especially farmers. The grain industry can gather information from other sources. And while farmers have an informal network, StatsCan “democratizes” market information – if it’s done right.

Because the StatsCan acreage survey was conducted 3-4 months ago when things looked very different, its estimates should be viewed with a lot of caution. Among pulse crops for example, spot bids for yellow peas have dropped 12% since mid-January while red lentil bids are up 9%. New-crop bids have slipped 2% for yellow peas and are up 5% for greens. New-crop red lentil bids are 16% higher than mid-January and large greens are 24% higher. Plus, prices for competing cereal and oilseed crops have also moved. Some of these changes are large enough to cause second thoughts about planting plans.

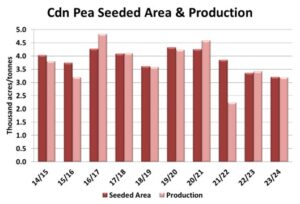

StatsCan reported 2023 pea plantings at 3.2 mln acres, 5% less than 2022 and well below the 5-year average of 3.9 mln acres. The StatsCan survey doesn’t ask for a breakdown of acres by type but, based on recent price spreads, green pea area could be steady while yellows are responsible for the drop in 2023 pea acreage. If the price behaviour since the StatsCan survey is any indication, total pea acreage could slip further and be closer to 3.0 mln acres.

Seeded area is just the first step in sorting out the 2023/24 outlook. Plugging an average yield into StatsCan acreage would mean a 2023 pea crop of 3.2 mln tonnes, about 400,000 tonnes less than 5-year average production. If so, supplies for the coming year would be the smallest (aside from 2021/22) since 2011/12.

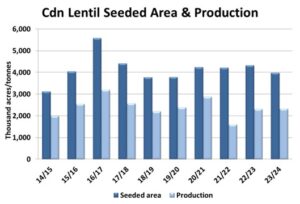

Seeded area of lentils was estimated by StatsCan just under 4.0 mln acres, 8% less than last year but close to the 5-year average. When we look at how lentil prices have strengthened since the StatsCan survey, actual plantings might end up closer to last year’s 4.2 mln acres. In this survey, StatsCan doesn’t ask farmers about the type of lentils they’ll be planting, but the price spreads mean a possible shift toward greens with fewer reds.

If we apply an average yield to this StatsCan acreage, the 2023 lentil crop would end up at 2.3 mln tonnes, almost identical with 2022 production and supplies would remain steady. It’s still very early, but export prospects for 2023/24 look solid again, which would keep prices well supported.

Seeded area of chickpeas was estimated at 260,000 acres, up 11% from last year but below the 5-year average of 318,000 acres. With an average yield, the 2023 crop would be 162,000 tonnes, 27% more than last year. That wouldn’t actually be heavy though, as a very small carryover means 2023/24 supplies would still be lower than the current year.

Pulse Market Insight provides market commentary from Chuck Penner of LeftField Commodity Research to help with pulse marketing decisions.