Pulse Market Insight #300

Indian Monsoon Outcome Key for Pulse Outlooks

We think it’s important to not react too quickly to weather events, and particularly forecasts. For example, the crop outlook in western Canada has already made a number of sharp U-turns, and it’s only mid-June. As we get further into the growing season, outcomes will become more certain and the outlook will become clearer.

Even though we don’t want to bet too much on weather forecasts, there is a potential situation in India that certainly bears watching. Recently, the Indian Meteorology Department lowered its rain forecast for the southwest monsoon season to 90% of the long-term average, based on the potential for a large El Niño event. This was the lowest IMD monsoon forecast in at least 20 years. The actual monsoon performance doesn’t always line up with the IMD forecast, but the accuracy of its forecasts seems to be better in recent years.

While there’s plenty of uncertainty in the forecast, it’s worth noting that back in 2014/15 and 2015/16, when India went through two consecutive shortfalls, its pulse imports rose sharply. Large import volumes continued in the following two years and pulse production in Canada and elsewhere rose in response to the high prices. Eventually though, those large imports built up in Indian warehouses and the government imposed import restrictions which caused volumes (and prices) to drop sharply. That lasted until 2023/24, when monsoon rains were below average again and India’s government dropped its tariffs.

This brief history lesson suggests that if Indian monsoon rains are well below average in 2026/27, Indian import demand could rise considerably. Whether that includes a drop in import tariffs – currently 30% for peas and 10% for lentils – remains to be seen. To a large extent, tariff decisions depend on pulse prices within India. If prices rise in response to its smaller pulse crops, the Indian government could try to keep food prices under control by lowering tariffs and easing the way for imports.

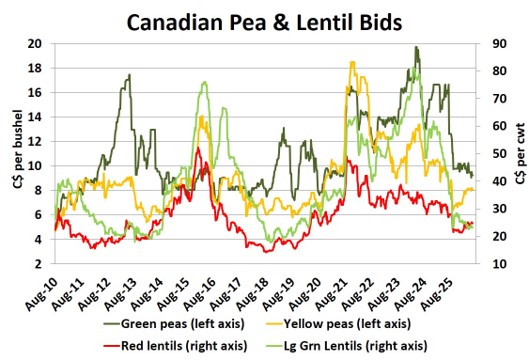

If Indian monsoon rains are deficient, Canadian pulse prices could see some improvement. Looking back over the last 15 years, we see the response in Canadian pea and lentil bids in 2014/15 and 2015/16. Keep in mind, the Indian market was responding to two consecutive years of poor monsoon rains, not just one. Back then too, Canada dominated global pulse trade with a lot less competition from other pulse exporters, which added to the upside. After that though, the high prices caused pulse production to rise sharply in western Canada and other countries, which caused prices to cycle lower.

Of course, pulse prices are influenced by numerous factors, not just Indian trade. For example, the sharp rally in 2021/22 occurred when India was restricting pulse imports and was mostly driven by the drought in western Canada.

Overall, a shortfall in Indian monsoon rains should benefit Canadian pulse prices but in crop markets, there are no crystal balls and no sure things. While a marketing strategy for 2026/27 could include waiting to see how the Indian situation develops and delaying some sales until later in the year, it’s important (as always) not to put all the “marketing eggs” in one basket.

Pulse Market Insight provides market commentary from Chuck Penner of LeftField Commodity Research to help with pulse marketing decisions.