Pulse Market Insight #288

Crop Prospects for 2026

This seems to be the time of year when there’s a flood of reports looking back at the past year or gazing ahead to the new year. While looking backward allows a person to gauge their grain marketing performance, hindsight generally doesn’t provide much help for making decisions about the upcoming year.

In fact, every marketing year is different. Making next year’s decisions based on last year’s successes or failures can be counterproductive. After all, acreage will shift and while there are always hopes for big yields, the odds of record output happening again in 2026 are very unlikely. In addition, global trade will also change (hopefully for the better) and affect next year’s market prospects.

This is also the time of year when we start thinking about farmers’ planting decisions for next spring. There are many factors going into those decisions, especially crop rotation considerations, but prices and profitability are also important. Typically, we use basic production costs and new-crop bids to compare gross margins for a number of crops. Of course, each farm’s farming practices and cost structure are different, so we use a set of generic production costs.

Often, new-crop bids are available for most crops by now, but this year’s heavy supplies seem to be decreasing buyers’ urgency for contracting tonnage for 2026/27, especially for special crops. This means we need to use our best “judgement” of where new-crop bids could show up.

This gross margin analysis isn’t the be-all and end-all of our acreage guesstimates though. We also spend time talking to people on the front lines to get farmer feedback and a few themes seem to be emerging for 2026. First, maintaining crop rotations is the most important driver and will limit the size of shifts in and out of various crops. At the same time though, on-farm inventories of some crops are much larger than others and could discourage acres of the “heaviest crops”.

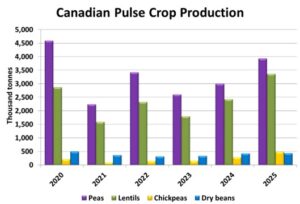

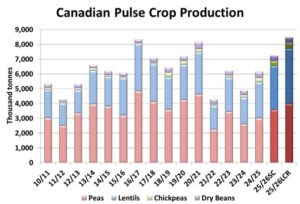

One other theme we’ve been hearing frequently is that seeded area of pulses will be trimmed, with peas mentioned most often. Ending stocks for all pulses will be historically large in 2025/26, meaning there will still be plenty of bins full of peas, lentils and chickpeas at seeding time. For some farmers, 2026 is seen as an opportunity to give pulse rotations a rest. That said, there aren’t other crops that are “big winners” in the 2026 acreage derby, and that could limit some of the losses in pulse acreage.

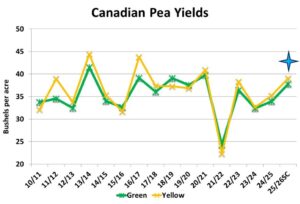

Our guesstimates include seeded area of peas slipping just below 3.0 mln acres, down 16% from last year. If so, it could be the smallest acreage base of peas since 2011 and would likely include reductions for all classes.

For lentils, we’re also looking at a decline in seeded area although not quite as severe at 3.9 mln acres, 11% less than last year and the lowest since 2023. We expect most of that decline would occur in green lentils, with very large supplies hanging over the market.

Acreage of chickpeas is also expected to slip by 12% to 475,000 acres. Even though chickpea prices continue to weaken, we’re still looking at historically sizable acreage as farmers have been having success growing chickpeas in the last few years.

Prices of black and pinto beans are somewhat depressed and we’re expecting that will allow dry bean acreage to also decline, although not as much as the other pulses.

Of course, these numbers are what we call “guesstimates”, which are a combination of analysis, feedback and a bit of gut feel. And if conditions change, especially with respect to trade barriers, the acreage projections could look a whole lot different.

If acreage of pulses does decline in 2026, we see that as a healthy and positive step. As the old saying goes, “the best cure for low prices is low prices.” Lower production is the way that markets recover from periods of depressed prices, a basic law of supply and demand. And if farmers in other countries do the same, it sets the stage for a price recovery in 2026/27.

Pulse Market Insight provides market commentary from Chuck Penner of LeftField Commodity Research to help with pulse marketing decisions.